The High Toll of Being Poor in the U.S.A.

"Georgia has long struggled to rein in payday lenders, but even ambitious regulations can’t always stop the predatory practice."

PHOTOGRAPH BY MARK DUFFY / ALAMY STOCK PHOTO

"Georgia has long struggled to rein in payday lenders, but even ambitious regulations can’t always stop the predatory practice."

PHOTOGRAPH BY MARK DUFFY / ALAMY STOCK PHOTO

Impoverished Americans face a myriad of problems unknown to the middle and upper class, the most significant of which are regressive costs.

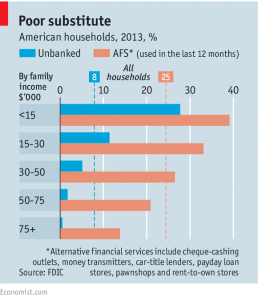

Officially, 14.8% of people in the United States live in poverty. Furthermore, 20% of Americans use alternative financial services to pay bills, get loans, and generally afford to live in the wealthiest country in the world. The most common alternative to a retail bank is a local check-cashing store, which charges a percentage fee on the cashed amount (for example, a store charges a 1.5% fee. This means that it will cost $15 to cash a $1,000 check). More affluent Americans that have enough money to escape minimum-balance fees of commercial banks can afford to open a personal account, while facing fewer risks of racking up high fees. On the flipside, as one might expect, the poor and less financially stable are more likely to incur banking fees, and 20% of customers pay a whopping 80% of all bank fees.

PHOTOGRAPH BY MARK DUFFY / ALAMY STOCK PHOTO

Since the early 1990s, the payday-loan industry has sprouted up in the place of retail banking, as banks have stopped operating in the short-term credit market. Due to the institution of new service fees and increasing penalties by commercial banks, many customers have switched to the industry that says it is looking out for the average American. Currently, almost 20 million households use payday loans to pay bills and purchase necessities, including food and medicine. However, this comes at a steep cost and with high interest rates. According to an article published by the Economist, the median loan in 2013 was $350, lasted two weeks, and charged $15 per $100 borrowed—an interest rate of 322%. Many Americans get stuck in a debt trap, taking out new loans to pay old ones, leaving them with ever-rising fees. Moreover, often desperate for quick cash, people will use their car or furniture as collateral.

Those Americans that receive tax refunds as a form of state welfare often use refund anticipation checks (RACs) to make their tax preparation fees deductible from their IRS refund. Low-income workers that cannot afford to pay their tax preparers often wait until they receive their benefits to repay their debt. RACs—which function as loans—often cost between $25 and $60 for short-term credit, and usually include additional fees. This inefficient system leads tax preparers to profit exorbitantly at the expense of vulnerable citizens who are simply trying to put their Earned Income Tax Credit to good use.

Less obvious costs associated with poverty include expensive local grocery stores and lower quality produce, as well as regressive taxes such as sales tax, fines, and expensive housing. Those without cars cannot always easily access more affordable chain grocery stores and must accept the steep price of buying lower quality food for more money. Further, though many Americans wish to purchase a house and pay a mortgage that is less than the cost of apartment rent, a market that is overvalued, they lack the credit and such the ability to pay a down payment. Therefore, they continue to rent relatively expensive apartments, a major long-term expense. Though not unique to poverty in the United States, the cost of sales tax weighs more heavily on the income of the poor than the wealthy, and even one parking ticket can set someone back weeks of disposable income. In 2014, almost half of American families reported an unexpected $400 expense would require them to sell property or take out a loan to pay it off.

Less obvious costs associated with poverty include expensive local grocery stores and lower quality produce, as well as regressive taxes such as sales tax, fines, and expensive housing. Those without cars cannot always easily access more affordable chain grocery stores and must accept the steep price of buying lower quality food for more money. Further, though many Americans wish to purchase a house and pay a mortgage that is less than the cost of apartment rent, a market that is overvalued, they lack the credit and such the ability to pay a down payment. Therefore, they continue to rent relatively expensive apartments, a major long-term expense. Though not unique to poverty in the United States, the cost of sales tax weighs more heavily on the income of the poor than the wealthy, and even one parking ticket can set someone back weeks of disposable income. In 2014, almost half of American families reported an unexpected $400 expense would require them to sell property or take out a loan to pay it off.

It’s hard to imagine so many people being in such a tight spot, having to be concerned with survival and maintenance of their household on an everyday basis. The credit and banking industry is propping up tens of millions of people who live in or on the edge of poverty. The modern financial system has ingeniously allowed us to develop new businesses, invest, see our wealth cultivated, and increase economic growth. However, credit and lending has also allowed people to overspend, misplace their money, and live in perpetual debt. Lending systems shouldn’t be a lifesaver for people that need to buy food, clothes, and pay their bills. They should be a lifesaver for entrepreneurs and generators of business. Our banking and financial services have certainly allowed millions of Americans to keep their heads above water but they have also allowed the nation to ignore the pressing issues of poverty and wealth distribution.

Unique to poverty in the United States, relative to other Western democracies, is a marked lack of worker benefits and employee friendly rights. Minimum wage jobs do not allow for workers to accumulate wealth or transition to a better-paying profession. Many people have no say in the hours they work and cannot manage to work a second or part-time job on the side. The reality that thousands of people with 40-hour workweeks are living in poverty and have a low standard of living is bad enough. The fact that politicians and major employers are not held accountable to improve the livelihood of hard-working, dedicated countrymen is even worse. Most concerning, however, is the lack of moral outrage in regards to the fact that CEOs of the top 500 American companies make 340 times the average production worker ($36,900), and is characteristic of America’s skewed mindset. In our society, excessive wealth and extravagance is lauded, while the hard work of thousands of workers is worth pennies to a CEO’s ideas and management skills. Caring for one’s own and blaming the poor for their situation is a natural reaction in the dog-eat-dog labor market.

The odds are stacked against those that work some of the longest hours and keep this country running. Most minimum wage or low-paying jobs without strong union support have no paid leave. Paid maternity leave is not guaranteed by the government, a feature we share with the likes of Papua New Guinea and a handful of other less developed countries. Over the last 30 years, wages and income have not increased for the poor and lower-middle class. Moreover, many issues the poor face come down to the horrific history of racism and the racial wealth gap in the United States. As white Americans have had better access to investment, major industries, and white-collar jobs for centuries, a serious racial wealth gap has arisen, persisted, and even deepened in the last 35 years. A significant factor to the U.S. system is the lack of equal opportunity. Sociologist Dalton Conley found through his research that the single greatest indicator of children’s economic future is the wealth of their parents. Wealthier families live in richer communities with better public resources and schools, and can afford better colleges, help pay for a house, or provide initial capital for a business. Conley also found that white households on the cusp of the poverty line often have a positive net worth of $10,000 to $15,000, while black households within the same income bracket instead have a negative net worth. Due to historical and institutional disadvantages toward wealth accumulation, coupled with steep debts and expensive mortgages for devalued homes, poor African Americans are often forced to rely on usurious lenders.

The criminalization of poverty is another issue facing the United States. In a yearlong investigation, NPR found that a fourth of misdemeanor convictions result in jail time, not for the crime committed, but instead for the failure of the defendant to pay court fees. Incredibly, in more than 40 states, defendants can be charged for their public defender and if convicted, can be charged for room and board, be billed for probation and parole services, and be charged a fee for the electronic monitor devices they are forced to wear. As the U.S.’ prison population has exploded in the last 40 years, costs of running jails, prisons, and courtrooms have likewise skyrocketed. Rather than increasing taxes, which is an unpopular choice for elected officials, state legislatures have increased fees defendants and the convicted must pay to keep the operation running. In one case, a defendant was even charged for the county fitness center. When defendants pay salaries and maintenance costs of the courtroom and county budget it becomes particularly difficult to distinguish between the purpose of conviction charges and fees—are convicted citizens paying the price for a serious crime or simply paying the price for the judiciary to continue its domineering operation and fund the bureaucracy?

In cases where the poor are apprehended and charged for traffic violations, petty robbery, vagrancy, and other minor, non-violent crimes, they are facing costs they cannot afford, and are thus jailed for the crime of being poor. As Ann Yantis, an attorney for the Michigan State Appellate Defenders Office, notes, “from the defense view, the sentence is meant to be punishment for the crime and to then say that we are going to charge you for the privilege of being prosecuted and sentenced for the crime is somewhat a double penalty.” However, because defendants and criminals are unpopular in the eyes of the public, state legislatures have been able to get away with charging them more and more in the place of raising taxes.

The United States has yet to embrace and support its poor and needy in the last half-century. Long considered a nation of opportunity, those unlucky enough to find themselves clasped in the grip of poverty face insurmountable problems that are unknown to the rest of American society. The lack of compassion and responsibility felt towards our fellow men and women has led the once prevailing welfare state to dwindle. The idea that everyone is responsible for their own welfare and wealth has been proven false yet again, most recently by the Great Recession, which pulled middle class families down and trebled the number of people using the SNAP program. The Great Recession, like many historic economic recessions, hurt the poor and minority groups the worst. Not only was inflation worse for the poor but African-Americans also lost half their wealth between 2005 and 2009.

The distaste for helping the poor in the U.S. is appalling. I would remind those Americans who dislike the idea of increasing taxes and closing corporate tax loopholes to pay for social programs and spending, that this country was largely built on the backs and with the blood of black slaves and neglected immigrants. These members of the underclass did not enjoy the privileges afforded to native white Americans, and to this day lack the respect they and their progeny deserve. I would also remind them what message is emblazoned at the base of the Statue of Liberty.

New Colossus

‘Not like the brazen giant of Greek fame,

With conquering limbs astride from land to land;

Here at our sea-washed, sunset gates shall stand

A mighty woman with a torch, whose flame

Is the imprisoned lightning, and her name

Mother of Exiles. From her beacon-hand

Glows world-wide welcome; her mild eyes command

The air-bridged harbor that twin cities frame.

“Keep, ancient lands, your storied pomp!” cries she

With silent lips. “Give me your tired, your poor,

Your huddled masses yearning to breathe free,

The wretched refuse of your teeming shore.

Send these, the homeless, tempest-tossed to me,

I lift my lamp beside the golden door!”’